Closing Disclosure Explainer

Use this tool to double-check that all the details about your loan are correct on your Closing Disclosure. Lenders are required to provide your Closing Disclosure three business days before your scheduled closing. Use these days wisely—now is the time to resolve problems. If something looks different from what you expected, ask why.

How to use this tool to review your Closing Disclosure: Below you'll see the actions you should take to review your Closing Disclosure and some handy definitions to know when you do.

The sample Closing Disclosure shows you where you'll find information on your own form. When you select any of the Closing Disclosure, the tool highlights this information on the image and also highlights the explanation. You can download the sample Closing Disclosure if you'd like to print it or just get a better look.

Sample Closing Disclosure

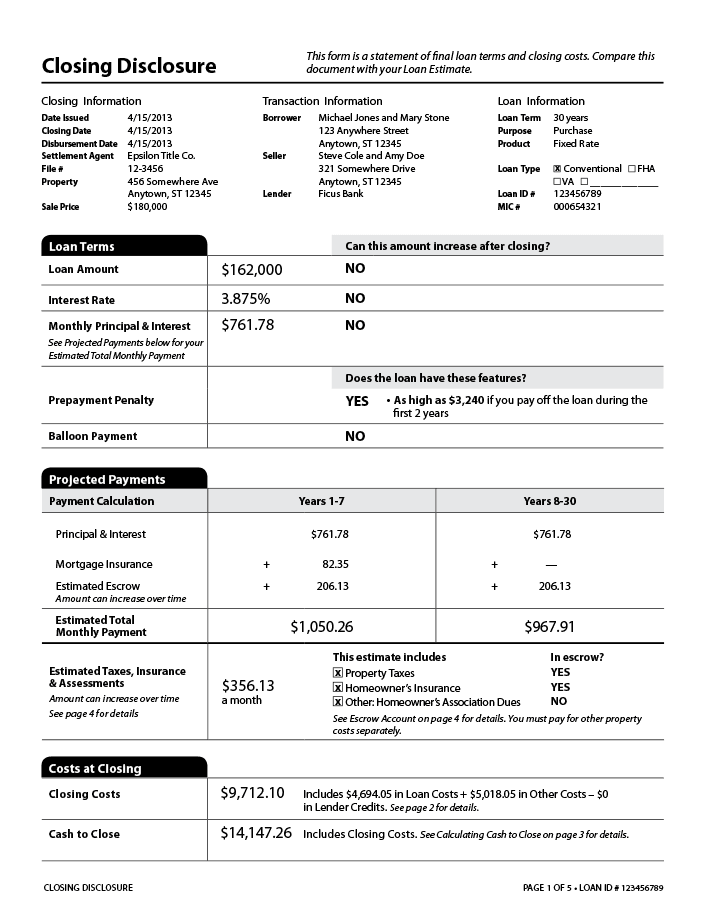

Check the spelling of your name

Check that loan term, purpose, product, and loan type match your most recent Loan Estimate

Check that the loan amount matches your most recent Loan Estimate

Check your interest rate

Does your loan have a prepayment penalty?

Does your loan have a balloon payment?

Check that your Estimated Total Monthly Payment matches your most recent Loan Estimate

Check to see if you have items in Estimated Taxes, Insurance & Assessments that are not in escrow

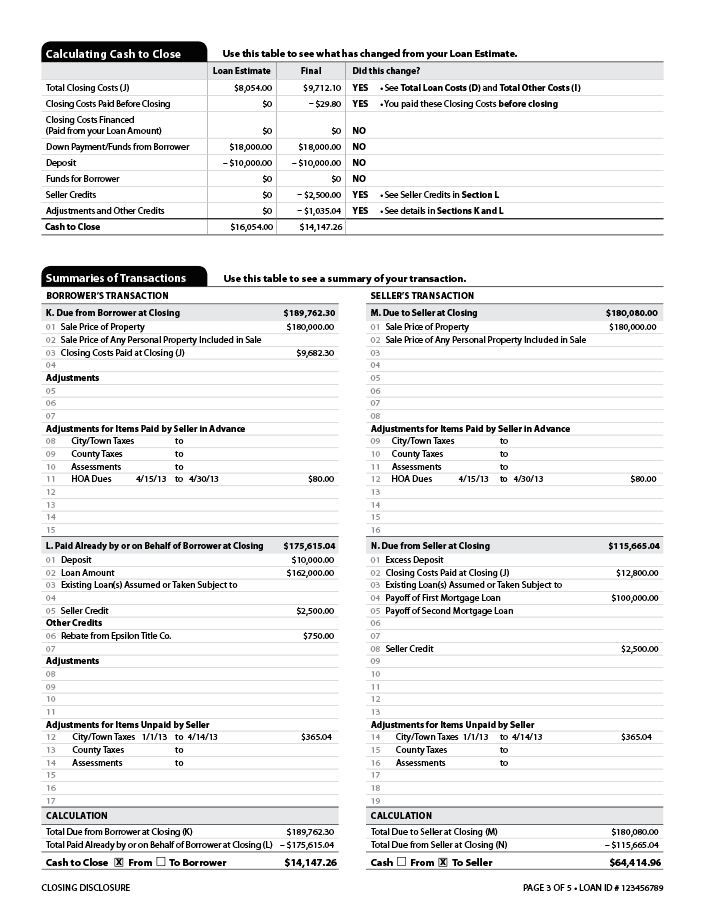

Check that your Closing Costs match your most recent Loan Estimate

Check that your Cash to Close matches your most recent Loan Estimate

Monthly Principal & Interest

Principal & Interest

Mortgage Insurance

Estimated Escrow

Check the spelling of your name

Check that loan term, purpose, product, and loan type match your most recent Loan Estimate

Check that the loan amount matches your most recent Loan Estimate

Check your interest rate

Does your loan have a prepayment penalty?

Does your loan have a balloon payment?

Check that your Estimated Total Monthly Payment matches your most recent Loan Estimate

Check to see if you have items in Estimated Taxes, Insurance & Assessments that are not in escrow

Check that your Closing Costs match your most recent Loan Estimate

Check that your Cash to Close matches your most recent Loan Estimate

Monthly Principal & Interest

Principal & Interest

Mortgage Insurance

Estimated Escrow

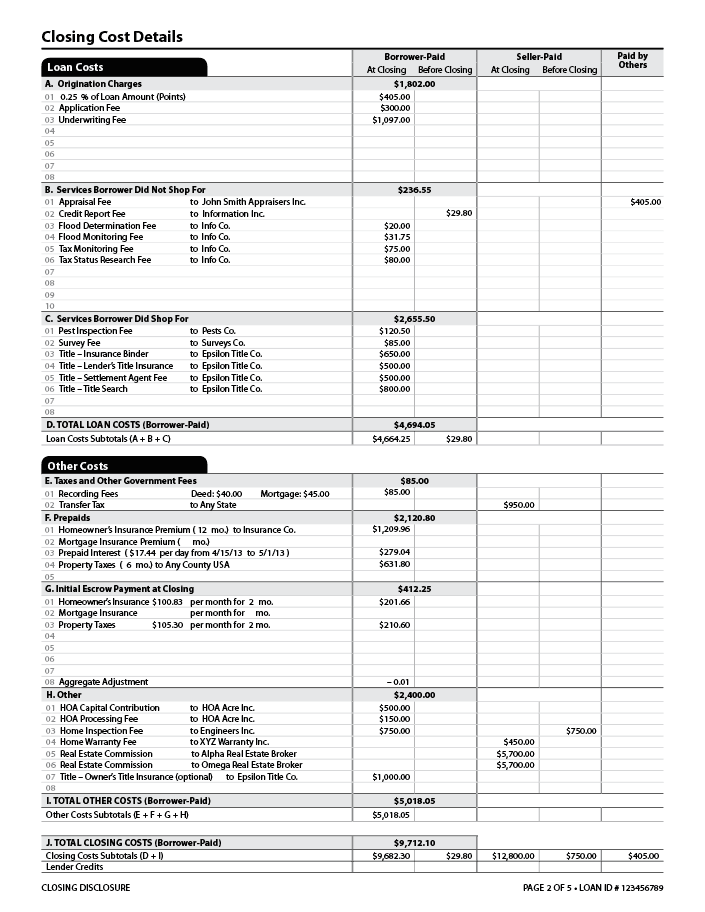

Check that “Services Borrower Did Not Shop For” are similar to what was shown on your Loan Estimate

Check that prices in “Services Borrower Did Shop For” match what you agreed to pay

Borrower-Paid

Origination Charges

Points

Taxes and Other Government Fees

Prepaids

Initial Escrow Payment at Closing

Other

Total Closing Costs

Lender Credits

Check that “Services Borrower Did Not Shop For” are similar to what was shown on your Loan Estimate

Check that prices in “Services Borrower Did Shop For” match what you agreed to pay

Borrower-Paid

Origination Charges

Points

Taxes and Other Government Fees

Prepaids

Initial Escrow Payment at Closing

Other

Total Closing Costs

Lender Credits